On August 7, 2024, the Korea Fair Trade Commission (KFTC) implemented amendments to the Monopoly Regulation and Fair Trade Act (MRFTA) on the reporting and review of mergers. These amendments to the MRFTA include (i) introduction of voluntary commitment procedure and (ii) expansion on the scope of exemptions to merger filing. Additionally, the amendment to the Merger Review Guidelines was implemented on May 1, 2024 to reflect the characteristics of the digital economy and the pre-notification procedure was stipulated in the Merger Filing Guidelines.

The following is a summary of these recent changes under the MRFTA on merger control in Korea.

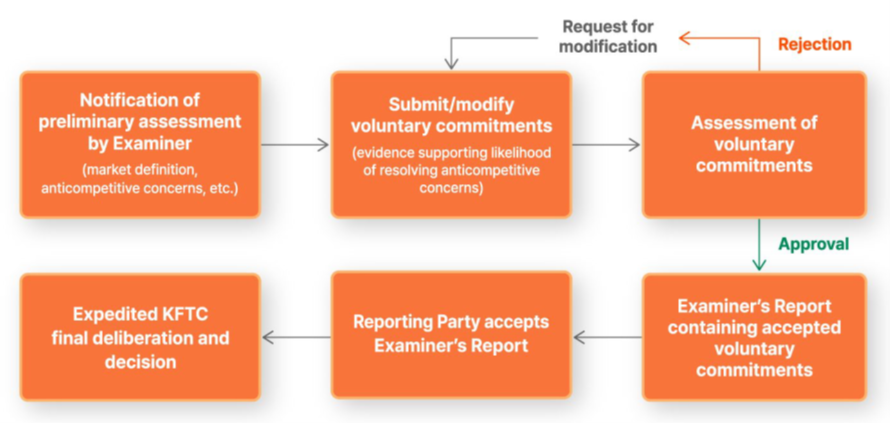

- Voluntary commitment procedure

The KFTC implemented a system for the submission of voluntary commitments in business combinations. In addition to amending the MRFTA, the KFTC enacted the Detailed Guidelines for the Operation of the System for the Submission of Voluntary Commitments in Business Combinations to set forth the voluntary commitment procedure in detail. Companies may benefit from this system as the KFTC’s review period can be shortened for a review of business combinations that are deemed to restrict competition. However, if the merging parties do not submit voluntary commitments, or if the KFTC does not accept the submitted commitments, the KFTC may impose its own remedies or block the business combination.

An overview of the system for the submission of voluntary commitments is illustrated in the table below.

- Notification of preliminary assessment: The KFTC Examiner notifies the Reporting Party of the preliminary assessment on the relevant sector (market definition, etc.), anticompetitive concerns and the direction of potential remedies through an in-person meeting.

- Submission of voluntary commitments: The Reporting Party, after consulting with the other party, submits the proposed voluntary commitments including detailed commitments and method of implementation and evidence supporting that the proposed commitments effectively resolve noted anticompetitive concerns and confirmation of implementation within a reasonable time period.

- Assessment of voluntary commitments

- The KFTC Examiner evaluates whether the proposed voluntary commitments adequately address the noted anticompetitive concerns and notifies the parties through an in-person meeting (KFTC may seek the opinions of interested third parties or experts, if necessary).

- If the KFTC Examiner concludes that the proposed voluntary commitments are inadequate, the Reporting Party may be requested to modify such commitments (up to 2 requests for modification). However, if there are unavoidable circumstances, such as significant difficulty in preparing voluntary commitments to meet the requirements of the KFTC, additional requests are permitted.

- The period of time spent modifying proposed voluntary commitments is not calculated as part of the KFTC’s overall merger review period (i.e., does not start the clock on the merger review).

- Issuing the Examiner’s Report: If the KFTC Examiner determines the proposed voluntary commitments adequately address the noted anticompetitive concerns, such commitments will be considered and drafted in the Examiner’s Report as acceptable remedies together with the KFTC Examiner’s opinion.

- Procedures for Deliberation/Decision: If the Reporting Party submits a written opinion confirming agreement with the Examiner’s Report without any objections, the KFTC will (i) hold a plenary session within 15 days (instead of the standard 30 days) from the submission of the written opinion and (ii) issue a written decision within 20 days (instead of the standard 35 days) from the conclusion of the plenary session.

- Expansion on the scope of business combinations exempt from merger filing obligation

The following are types of business combinations that are exempt from merger filing obligation following the expansion of exemptions by the KFTC under the amended Merger Notification Guidelines and Merger Review Guidelines:

| Business combination type subject to merger filing exemption | Details on exemption |

| Establishment of PEF | l The establishment of a private equity fund refers to investment where the investor will be the largest shareholder of the PEF.

l However, when an established PEF engages in M&As and the filing thresholds are met, merger notification is still required. l The establishment of a special purpose company by a PEF still has a merger filing obligation. |

| Less than 1/3 of interlocking directors | l An interlocking directorate involving less than 1/3 of directors of the counterparty is exempt from filing as there is difficulty in the interlocking directorate having influence on major decisions of the counterparty. However, merger filing is still required if the representative director is one of the interlocking directorates. |

| Statutory mergers or business transfers between the parent company and subsidiary | l Statutory mergers or business transfers between the parent company and a subsidiary under the Commercial Code (a company with shares exceeding 50% of the total shares issued in another company is a subsidiary) are exempt from merger notification as such transactions are unlikely to cause new anticompetitive concerns. |

| Mergers between affiliates with respective values less than KRW 30 billion | l Prior to the amendment to the MRFTA, in case of statutory mergers and consolidation between affiliates, the assets and worldwide sales of the counterparty company to be merged or consolidated were included. As this may result in the double-counting of the assets and sales of the merged/consolidated entity, the amended MRFTA provides that the assets and sales of the merged entity will be calculated on a non-consolidated basis (and not on a consolidated basis). |

| Transfer of assets or business under KRW 10 billion | l The merger notification threshold for the transfer of a business or assets has increased to KRW 10 billion (from KRW 5 billion) or 10% of the total assets of the transferring company. |

- Amendment of Review Guidelines to reflect the characteristics of the digital economy

On May 1, 2024, the KFTC implemented the amended Merger Review Guidelines to reflect and account for the characteristics of the digital economy and provision of free services by large online platform operators, among others, which were factors difficult to account for prior to the amendment.

| Amendment | Contents of Amendment |

| Subject of simplified merger review | l M&As involving online platform operators are subject to simplified merger review if it is (i) a conglomerate merger and (ii) the service provided by the online platform is not complementary or a substitutable.

n However, if the average number of monthly users of the target (in the case of business transfers, the transferred business) in the immediately preceding year of the year which the filing occurs exceeds 5 million (counted by unique users, multiple visits by the same user are not counted) in Korea, the transaction is subject to a general merger review. l Transactions where a limited partner (LP) in a private equity fund (PEF) participates in the capital increase of the PEF or acquires the shares of another LP, is subject to a simplified merger review. |

| Defining relevant markets | l For multi-sided services that facilitate interactions between different user groups, multi-sided markets may be defined as separate markets for different user groups or a single market.

l For business combinations between entities that provide free services (i.e. compensation provided by means other than monetary payment), the relevant market may be defined based on demand substitution resulting from a decrease in service quality rather than change in price. l The combination of businesses whose activities involving innovation, such as R&D, which are essential or active, may be defined as an “innovation market” considering that the companies are competing in terms of innovation rather than price. Examples of the innovation markets listed in the amendment include competition in the development of semiconductor manufacturing devices and operating systems (OS) for smart devices. |

| Evaluating restrictions on competition | l When reviewing a business combination between online platforms, the strength of direct and indirect network effects of increasing the number of users or scale of data is considered in determining the business combination’s restriction of competition.

l In evaluating the restriction on competition for the provision of nominally free services, as it is difficult to calculate the market share based on sales because services are provided nominally free, the market share is calculated using alternative variables such as number of users and frequency in the use of the service. l In evaluating the restrictions on competition in conglomerate mergers, as there is the potential to engage in tying or bundling products, the Merger Review Guidelines added a new criterion to assess the potential bundling effect of a conglomerate merger. |

| Examples of increased efficiencies that consider the unique characteristics of the digital economy | l The increase in service users from the business combination that may increase the benefits for existing users through direct or indirect network effects.

l The use of additional data obtained from business combinations may be used to create innovative services or reduce the costs of the production or distribution process. l Business combinations may broaden the range of services available to users and increase consumer benefits. l For business combinations involving innovative digital tech startups, the exit of existing input capital may result in creating new startups and entry into the market that could significantly activate the startup ecosystem in Korea. |

- Pre-notification procedure

Prior to the implementation of the pre-notification procedure for merger filings (Pre-notification) on August 7, 2024, the relevant parties were able to discuss whether a transaction was reportable or about the filing formalities (e.g., whether notifiable as a share acquisition or the establishment of a new company) of a transaction, while substantive issues regarding the filing were not included in such discussions. Citing the need to reduce the merger review period and prevent the issuance of unnecessary requests for information during the course of merger reviews, the KFTC amended its Merger Filing Guidelines to specifically state that for transactions involving complex transaction structures or multiple relevant markets subject to ordinary merger filing, which as a result may cause the parties difficulties in preparing a merger notification, the parties may consult with the KFTC by email prior to the submission of the merger filing. The KFTC released the following details regarding Pre-notification:

-

- The relevant parties can use Pre-notification not only for ordinary merger filings but also for simplified merger filings.

- There is no specified time period for Pre-notification. However, the parties must initiate Pre-notification at least 2 weeks prior to the filing.

- The merger filing can be submitted at any time, even after Pre-notification has been initiated by the parties.

- The parties are required to submit to the KFTC documents needed for consulting with the KFTC, but are not required to submit information that is not necessary for a substantive analysis (e.g., financial figures) or data requiring a substantial amount of time to prepare (e.g., market information); Such information can be submitted to the KFTC in the merger filing.

- The KFTC will notify the results of the Pre-notification by email.

- The KFTC will ensure and maintain consistency between the results of the Pre-notification and merger review, barring a significant change in the factual background or market status.